The three real risks to retirement

And why the usual approach misses all of them

When you first meet with a financial adviser, one of the topics that you will end up discussing is investment risk. For most people, it feels natural to view investment as something that is inherently risky and should be approached with caution. The messages you receive during your lifetime will only reinforce this feeling. The reality for most of us, though, is that in order to meet our financial goals, we have to invest our assets. The big challenge is how to understand exactly what risk is and how this applies to your own individual circumstances.

If you've had any previous dealings with an adviser, it’s likely that you've had to complete a risk questionnaire. These documents will ask you how you feel about investment risk and will provide an outcome that is supposed to match your own individual circumstances. Unfortunately, from our perspective, there are two fundamental failings in these questionnaires.

Firstly, they view risk as a single entity

You will be somewhere on a sliding scale, usually numbered from 1 to 10. By the very nature of these questionnaires, it’s likely that you’ll come out either around the middle or just it. The vast majority of people fill in these questionnaires in a cautious manner - nobody wants to risk losing all their savings. But our view is that risk is not a single thing. There are different types of risk, and they all affect people in different ways, based on their own individual circumstances and stage of life.

Even worse, these risk questionnaires were never built to benefit you. They give your adviser a number they can hang their hat on. If you end up with a risk score of four, then they can plug this number into some clever software and come up with a portfolio that supposedly matches this number. This portfolio takes no account of your own circumstances, just your answers to a questionnaire. If the portfolio doesn't help you achieve your financial goals, there's nothing you can do. You agreed with your adviser that you were a certain score, and they made you that score, regardless of whether or not it will help you get where you need to be.

We firmly believe that the best way to think of risk is the three main areas that can affect you during your retirement.

1. Permanent capital loss

This is the risk that we all worry about. Losing your money and never getting it back would be devastating for your future financial plans. We've all heard stories of someone who invested money and lost it all. But the reality is that permanent capital loss is very rare and is also very easy to avoid.

It sounds very simple, but the only way you can lose all your money is by having all your eggs in one basket. If you only own one or two assets, regardless of what they are, these assets could go wrong and become worthless. By having a diverse portfolio with either hundreds or ideally thousands of different assets, you completely remove the risk of permanent capital loss. Some assets may still go wrong, and you may lose the money invested in them, but you'll be protected by the sheer number of assets that you have.

2. Inflation

This is the one almost nobody talks about - and for most people, it's the biggest risk of all.

The only way to think about money is what you can buy with it - it's purchasing power.

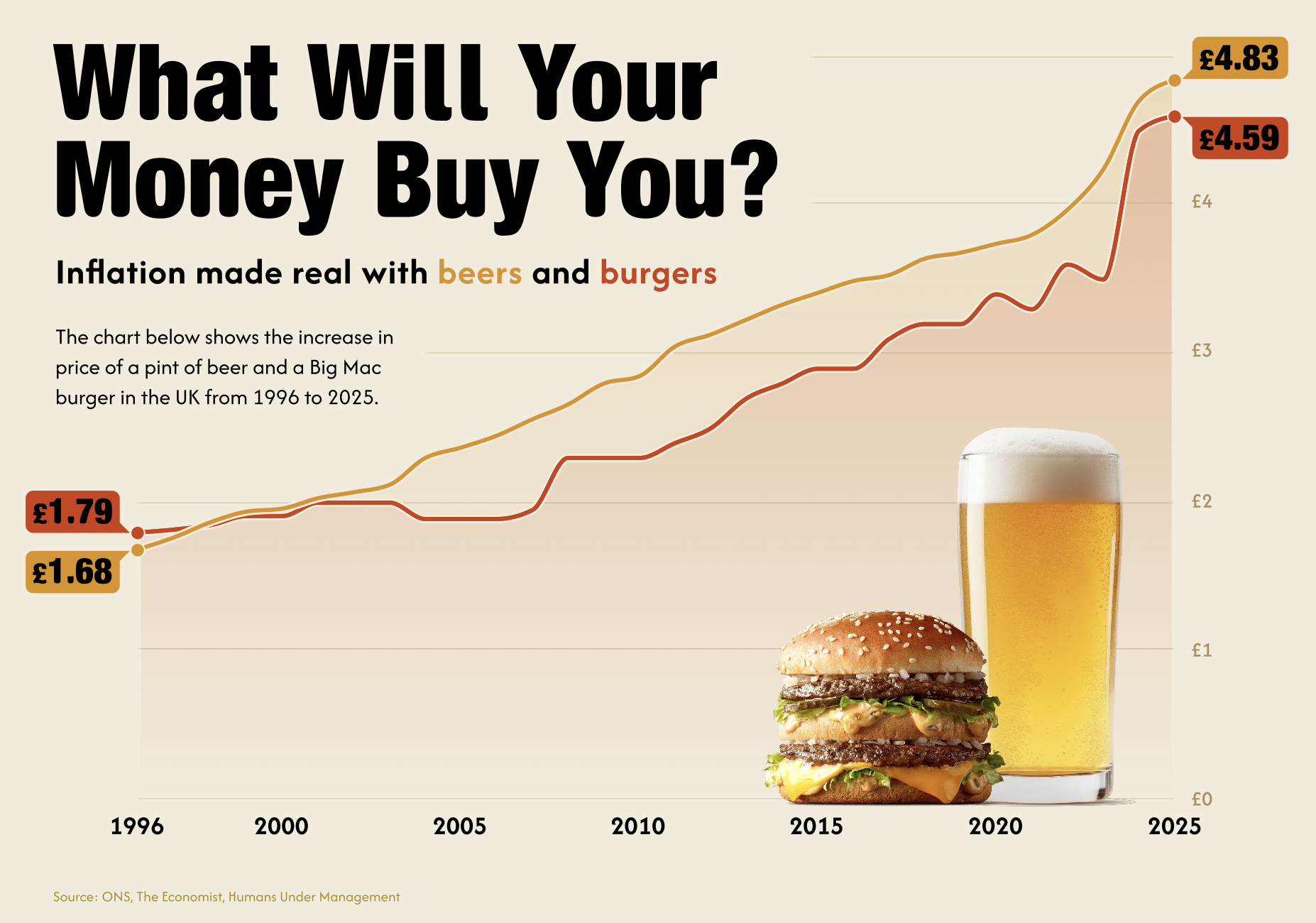

Inflation reduces the purchasing power of money over time, which means the same amount of cash buys fewer goods and services. The example I usually share is that over a 30-year period, an average annual inflation rate of roughly 4%, such as that tracked by the Office for National Statistics, reduces £100 of cash to about £30 in real spending power. Most clients I work with have a 30-year timescale for retirement so it’s important they beat inflation.

Assets that are viewed as safe, such as cash savings, rarely beat inflation. They provide certainty that they won't fall in value, but over time they are able to buy less. Over a typical 30-year retirement, this loss of purchasing power can lead to you running out of money. Your safe assets are actually the thing that kills you financially in the long term.

You may have income in retirement that is guaranteed and inflation-proofed, but not everybody is in this position. To ensure that you never run out of money, your assets need to beat inflation.

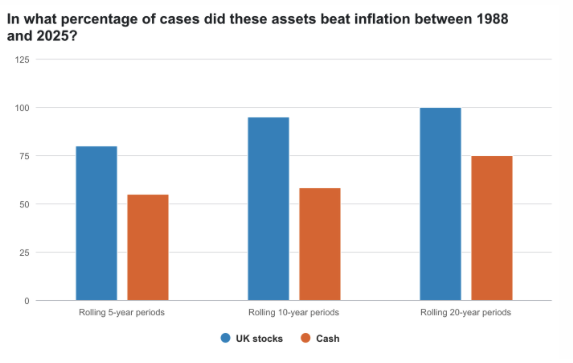

There's only one proven way to do this over the longer term, and that’s by maintaining exposure to growth assets such as equities. Equities (or ‘stocks’) have historically outpaced inflation, delivering positive ‘real’ returns that protect purchasing power far better than holding cash, which makes them the natural engine for the part of your income your guaranteed sources can't cover on their own.

The catch is that they don't grow in a straight line, which brings us to the third risk.

3. Volatility

This is the one everyone mistakes for risk: it isn't.

Volatility is simply the random short term up-and-down movement of all assets. It's behind every warning you've ever read - "past performance is no guide to the future," "investments can go down as well as up." All true. But going down and then back up is not the same as losing money. It just feels like it.

Most of this movement is driven by emotion in the short term, but it's unpredictable and there's a trade-off to be made when you invest money.

So here's how I'd ask you to think about it instead: assets that don't move much don't make much - they're low-return assets. Assets that move around more are the ones that build real wealth over time - they're high-return assets. If I stopped asking clients "How much volatility can you bear?" and instead asked "Would you like high-return or low-return assets in your portfolio?" - everyone would pick high return. Same question, but better framing.

And it gets easier still when you remember what you actually own. An equity portfolio isn't a casino chip. It's owing part of the best companies in the world - the Apple products in your house, the supermarket you shop in, the businesses you use every day. Owning them isn't a gamble. It's ownership.

The real damage volatility does isn't the dramatic one, either. Yes, a few people panic and sell when markets drop 30% in six weeks, as they did in 2020 - but advised clients rarely do that. The far more common harm is this: when the news is noisy and markets are jumpy, people assume the worst about money they haven't even looked at. They stop spending, cancel the holiday, or they don't help the kids. They shrink their lives to feel safe - and that's the real cost.

That's why at Callidus, we don't pretend volatility away – we plan around it. A safe pot to draw on, so you never have to sell good assets at a bad moment, and a growth pot doing the long-term heavy lifting (see the inflation point above). Managed properly, volatility stops being something to fear and becomes the engine of your retirement.

The point I feel strongly about

When you treat risk as a single line on a questionnaire, almost everyone ends up in the same cautious middle. It feels prudent, but it also moves people out of the assets that beat inflation and into the ones that don't, and over a 30-year retirement, that can cost you far more than a bumpy year ever could.

The middle of the road might feel safe, but more often than not, it isn't.